Overshooting of the Egyptian pound against the US dollar continues 8 months after the Central Bank of Egypt’s (CBE) decision to liberalise the foreign exchange system in November, despite some $8.4bn of portfolio inflows, according to a report published by HC Securities & Investments.

HC Securities & Investments analysts calculate that the fair value of the Egyptian pound against the US dollar should be reduced by 27% from the current value of EGP18.12 for every US dollar. The estimates are based on the mean reversion of the real effective exchange rate (REER) index.

Moreover, the overshooting could have initially been explained by the short-term supply-demand dynamics. However, the sizable portfolio inflows in recent months, with $54bn of fresh funds flowing into the system since the flotation of the currency in November should have moved the value of the Egyptian pound closer to its fair value, said the report.

From HC Securities & Investments’ point of view, the CBE is favoring an undervalued, yet stable currency over a volatile exchange rate, as evident by an increase in non-reserve foreign currency deposits to $5.86bn by the end of May, the report indicated.

From HC Securities & Investments’ point of view, the CBE is favoring an undervalued, yet stable currency over a volatile exchange rate, as evident by an increase in non-reserve foreign currency deposits to $5.86bn by the end of May, the report indicated.

Although the negative implications that would be associated with a volatile exchange rate is understandable, the current CBE policy is not helping with containing inflation and partially limits the transmission mechanism of the bank’s monetary policy tools, said the report.

Consequently, HC Securities & Investments advocates a gradual appreciation of the Egyptian pound in order to eliminate the existing overshooting by the first quarter of FY 2018, when Egypt’s current account starts to reflect more sustainable foreign currency inflows, mainly driven by the oil trade balance and tourism receipts.

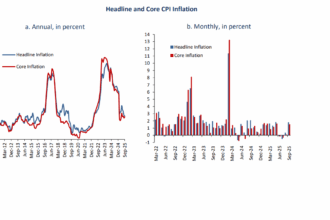

The current sky-rocket high inflation levels that registered at 30.9% in June can no longer be fully explained by cost-push factors. It is estimated that only 12% of the total 24% increase witnessed in the consumer price index (CPI) since October, which can be explained by the currency movement, according to the report. Such estimates are based on the percentage of imports to other GDP constituents, namely final consumption, gross capital formation, and exports.

On the other hand, total domestic credit growth has been largely flat since November. The Egyptian government has been expanding heavily on foreign debt, which HC Securities & Investments believes could have a similar impact on inflation.

Moreover, the report indicates that the single largest borrower in the market shows almost no elasticity to interest rate movements, thus any efforts to contain prices in the short term should be played through the exchange rate.

On the other hand, private business and household credit expansion have only been modest at 5% and 3%, respectively; consequently any further interest rate hikes would significantly risk growth, while on the long term, HC Securities & Investments forecasts that the government’s fiscal consolidation efforts will have a positive impact on inflation.

On the other hand, private business and household credit expansion have only been modest at 5% and 3%, respectively; consequently any further interest rate hikes would significantly risk growth, while on the long term, HC Securities & Investments forecasts that the government’s fiscal consolidation efforts will have a positive impact on inflation.

In regards to inflation estimates and forecasts, the report expects inflation to register an average of 24.0% in FY17/18, as a result of the budget-deficit to GDP dropping to 10.0% from 11.5% in FY16/17. Meanwhile for FY18/19, HC Securities & Investments expects inflation to reach an average of 12.0%, with the budget deficit further dropping to 8.3%. Persistently high inflation would keep private consumption growth depressed, as well as erode the Egyptian pound’s competitiveness, negatively impacting the country’s external position. The report estimates an average EGP/USD rate of 15.72 in FY17/18 and 15.38 in FY18/19.

Egypt’s total medium and long-term public and publicly guaranteed debt services stood at $32.7bn, which are divided into $2.88bn in the second half of FY 2016/17, $7.71bn in FY17/18, $12.76bn in FY18/19, and $9.35bn in FY19/20.

While excluding some $16.10bn of GCC deposits, medium and long-term public and publicly guaranteed debt services would stand at $16.59bn divided into $2.66bn in the second half of FY16/17, $5.23bn in FY17/18, $4.00bn in FY18/19, and $4.70bn in FY19/20.

Furthermore, the total short-term debt service stood at $12.16bn, of which $8.40bn is to be paid in the first half of FY17/18. Short-term debt includes $3.20bn loans from the African Export-Import Bank, the $2.00bn CBE repurchase agreement transaction, and the $2.59bn CBE currency swap agreement with China, all of which are fair to assume to be either public or publicly guaranteed.

This leaves total public and publicly guaranteed debt services in 2017 at $13.16bn.

This leaves total public and publicly guaranteed debt services in 2017 at $13.16bn.

The report concludes that in the short term, Egypt’s external position and investments are the key GDP growth drivers. HC Securities & Investments forecast that the current account deficit would drop to $14.3bn or 5.4% of GDP in FY17/18, compared to $16.6bn or 9.5% of GDP in FY16/17, before further narrowing down to reach $12.1bn or 3.8% of GDP in FY18/19, due to the improvement witnessed in Egypt’s oil trade balance, higher exports, and a partial rebound in tourism receipts to pre-revolution levels.

Moreover, GDP growth is estimated to reach 4.0% in FY16/17, corrected from the 3.5% that was forecasted previously, and to reach 4.4% in FY17/18, up from 4.0% previously. In FY18/19, HC Securities & Investments expects real GDP growth to accelerate to 4.9% on the back of a recovery in private consumption as inflation moderates and unemployment drops.